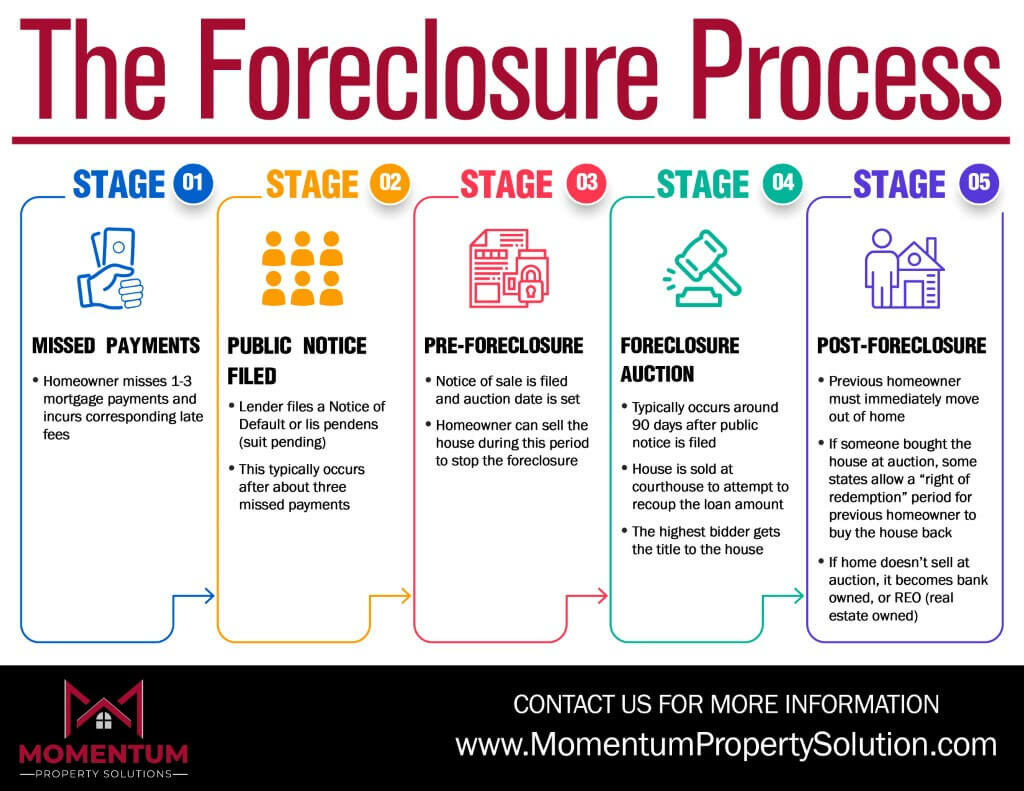

Foreclosure is when you are unable to keep up with making your monthly mortgage payments on your home. This situation then allows the lender to seize your property, evict you, and then sell the home and keep the proceeds from the sale. This is all stipulated in the mortgage note that you signed.

Facing foreclosure is a scary and unsettling time for homeowners. It can be difficult to determine what options you may have; much less deciding which one works best for your situation. There are a number of steps you can take when you’ve fallen behind on your payments. Housing counseling is available to help you determine which steps make the most sense in your situation.

With today’s volatile job market and economic problems due to the pandemic, home foreclosure is at an all time high. Many people believe that the banks don’t care if you have just lost your job or if you have suddenly become ill, and believe that regardless of the reason, failure to pay your mortgage will result in the foreclosure of your home.

It may be true that banks don’t care about you personally, but they definitely care about your money. There are a few important things that you should know if you feel as though foreclosing is a possibility. We’ll share some advice and tips to help you avoid foreclosure.

Step 1 – Talk to your lender today:

It might seem scary but when you realize that you’re going to have trouble making your mortgage payment, contact your lender and tell them about your financial difficulties. This gives them the chance to work with you to create a game plan that you can afford and manage. Don’t stop paying your bills altogether, and don’t wait until you can’t make payments before you do anything about it. Though you may feel afraid or embarrassed, immediately begin working with your lender to avoid foreclosure.

Get Started With a Free Debt Analysis

We make it easy on mobile or desktop. FREE with no obligations.

Banks are usually willing to work with homeowners to find a way to keep you in your home. Be honest with your lender about your financial situation and your ability to continue making payments in the future. A loan modification that either spreads out the missed payments or adds them to the end of the loan may be all you need to bring your loan current and keep you from losing your home. However, you won’t know for sure unless you talk to your lender and the sooner the better.

Step 2 – Call a nonprofit housing counseling agency:

A housing counseling agency can let you know your options and get you in touch with organizations that are specifically there to help save people’s homes. The call to a housing counseling agency is always completely free and confidential. The federal government offers several programs, such as the Home Affordable Refinance Program (HARP), to help homeowners refinance their mortgage into a low fixed-rate loan that could make your housing payment more affordable. This program is meant to help people who are current on their payments but anticipate problems in the near future. This government program is set to expire soon, so it’s important to act quickly if you want to take advantage of this opportunity. There are special protections afforded to active-duty military members through the the Servicemember’s Civil Relief Act (SCRA).

More tips and advice to prevent foreclosure:

- The bank does not WANT your house; they want you to keep your loan. Your lender will work with you and your credit counselor to find a way to work with you so that you can make your mortgage payments on time. This is one important thing that people don’t realize, and it is an excellent reason to enlist the aid of a credit specialist who knows how to talk to banks on your behalf.

- If you contact your lender immediately after you realize you have a problem, they will be less likely to force you to foreclose, and will instead try to help you adjust to whatever new situation has arisen that will keep you from paying your mortgage payments on time. Showing that you are responsible helps a lot.

- Fully understanding your foreclosure prevention options is key! There are many resources out there that you can use to find out about foreclosure prevention, but many of these sources are technically written. It helps a lot to have a credit counselor who is familiar with the process by your side as you figure out how to avoid foreclosure.

- You can use your assets to subsidize mortgage payments, and you can also delay payment on credit cards and other non-secured debt. This is a fine line to walk, though. You have to be careful that you do not mismanage other debt in order to successfully pay your mortgage. A housing counseling agency that also provides credit counseling is invaluable at times like this because they can help you avoid a hike in interest rates and other problems that arise from delaying credit card payments.

If you can’t afford to stay in your home:

If you have come to the conclusion that you cannot afford to stay in your home, you will want to take steps to minimize the damage to your credit. Selling your home is the best option, as this may allow you to pay your loan balance and even provide the funds for a new, more affordable home. However, if you are underwater on your mortgage, a short sale is a better choice than foreclosure. In a short sale, the bank agrees to sell the house for less than what you owe. Be sure this agreement addresses how you will handle the remaining balance on the home.

Filing for bankruptcy will give you temporary relief from the phone calls and letters from your lender and other creditors. It could also give you time to restructure your other debts so you might be able to stay in your home, but bankruptcy laws do not allow you to modify your current loan. Ultimately, in order for bankruptcy to allow you to stay in your home, you must be able to prove that you can continue making your existing payments.

Another option is to simply turn the home over to the bank. Known as deed-in-lieu-of-foreclosure, choosing this path does mean you will lose the home but it won’t be reported to the credit bureaus as a foreclosure and is therefore not as damaging to your financial future. Often, when it obvious you will not be able to maintain ownership of the home, banks would prefer this route, as it prevents a lengthy eviction process and could allow the bank to get the house sold more quickly.

When facing a financial crisis that could cost you your home, the important thing is to act quickly while you still have plenty of options. Housing counseling is a good place to start. Trained professionals can help you understand what your choices are and which options make sense for your current situation. They can also assist you in finding the right help to either save your home or minimize the financial impact of losing your home.

Conclusion –

Your home is your biggest investment and probably your most costly possession. Outside of health care, making your mortgage payment should be your absolute first priority. Home foreclosure is devastating in many ways. Not only are you displaced and all the money you have poured into paying your mortgage is wasted, but you lose a house that you have invested a lot of time, money, and emotion into.

Learn how to work with your housing counseling agency and your lender to avoid losing your house. You can avoid this tragedy and regain control of your finances by becoming actively involved and finding out as much as you can about the foreclosure process and how to avoid it.